Many renters are under the impression that their landlord’s insurance policy will cover their belongings, unfortunately that generally is not the case. Your landlord’s policy covers the building itself, but it may not include your personal belongings, and may not cover injuries sustained within the structure. That’s where renters insurance comes in.

Renters insurance protects your personal property in a rented apartment, condo or home from unexpected circumstances such as theft, a fire or sewer backup damage – and will pay you for lost or damaged possessions. It can also help protect you from liability if someone is injured on your property.

Renters insurance is similar in scope to homeowners insurance, with the exception that it does not provide coverage for the dwelling itself or other structures.

How does renters insurance work?

If you experience a covered loss in your rented space, renters insurance can help to cover the associated costs. The amount covered will depend on the type of loss that occurred and the amount of coverage you have.

There are two types of coverage options under a typical renters policy: Actual Cash Value coverage and Replacement Cost coverage. Here’s the difference between the two:

-

Actual Cash Value coverage will reimburse you for the value of the items at the time of the damage or loss.

-

Replacement Cost coverage covers the cost it takes to replace the items lost or damaged.

What does renters insurance cover?

A renters insurance policy offers you coverage for the loss or destruction of your personal belongings in the event of a covered peril such as:

-

Fire

-

Lightning

-

Windstorm

-

Hail

-

A frozen plumbing system

-

Theft

-

Vandalism

-

Impact by a vehicle

Renters insurance may also cover you if:

You are forced to temporarily move out of your home: In the event your home becomes unlivable due to damage caused by a covered instance such as a fire or vandalism, renters insurance can help cover the cost of alternative living arrangements while your home is repaired or rebuilt.

A person is injured on your property and requires medical attention: Personal liability coverage is designed to protect you, as well as other individuals who visit your home, if an accident were to occur. This type of coverage will help pay for medical costs and legal fees that you could end up incurring.

Items you keep inside your car are damaged or lost: Depending on your renters insurance policy, you may be covered for belongings that you keep inside your car. Note that this coverage does not include equipment or systems installed in the car.

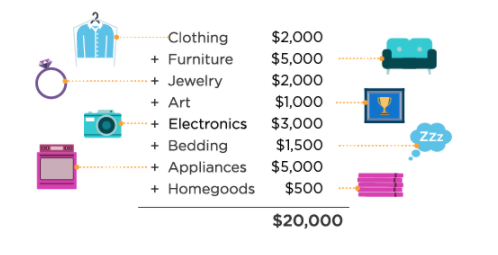

Here’s an idea of what covering the basics may look like from our friends at Nationwide:

What does renters insurance not cover?

Now that you have a basic idea of what renters insurance covers, it’s important to understand what a basic renters insurance policy does not cover so that you’re prepared:

-

Valuables. Expensive collectables and valuables such as jewelry may not be covered under a basic renters policy and may require additional coverage.

-

Home business. Operating a small business out of your home doesn’t mean it will be covered by your renters insurance. For instance, if your business laptop is stolen from your apartment, there’s a chance it could be considered business property and therefore, won’t be completely covered by your renters insurance. Check with your provider to see if your policy covers a home business or if you need additional coverage.

-

Motorized vehicles. Use or ownership of a motor vehicle will not be covered by your renters insurance even if it is parked on your property (this also applies to aircraft and specific watercraft). Personal belongings kept inside the vehicle, however, are typically covered.

Have questions? Do you need renters insurance?

Click here or on the image below.

Source: Nationwide