Business insurance audits can feel overwhelming, but they are essential for maintaining accurate coverage and ensuring fair premiums. For small business owners and HR managers, understanding the purpose and process of different audits, such as general liability and workers’ compensation, can be game-changing. These audits directly impact your bottom line by preventing overpayment or underpayment for insurance coverage.

This blog breaks down the key differences between general liability insurance audits and workers’ compensation audits, showing you how they operate, what they cover, and how to prepare effectively. By the end, you’ll know how to approach these audits with confidence and clarity.

key takeaways

-

General liability audits verify revenue, subcontractor costs, and employee counts to ensure your premiums reflect actual risk exposure.

-

Workers’ compensation audits confirm payroll totals and employee classifications to prevent misclassification errors, penalties, or coverage gaps.

-

Accurate reporting during audits protects your business from unexpected costs and ensures fair premiums.

-

Preparation is key—organized records, communication with your insurer, and checklists help streamline the audit process.

-

Annual policy reviews keep your coverage up to date with your business’s growth and operational changes.

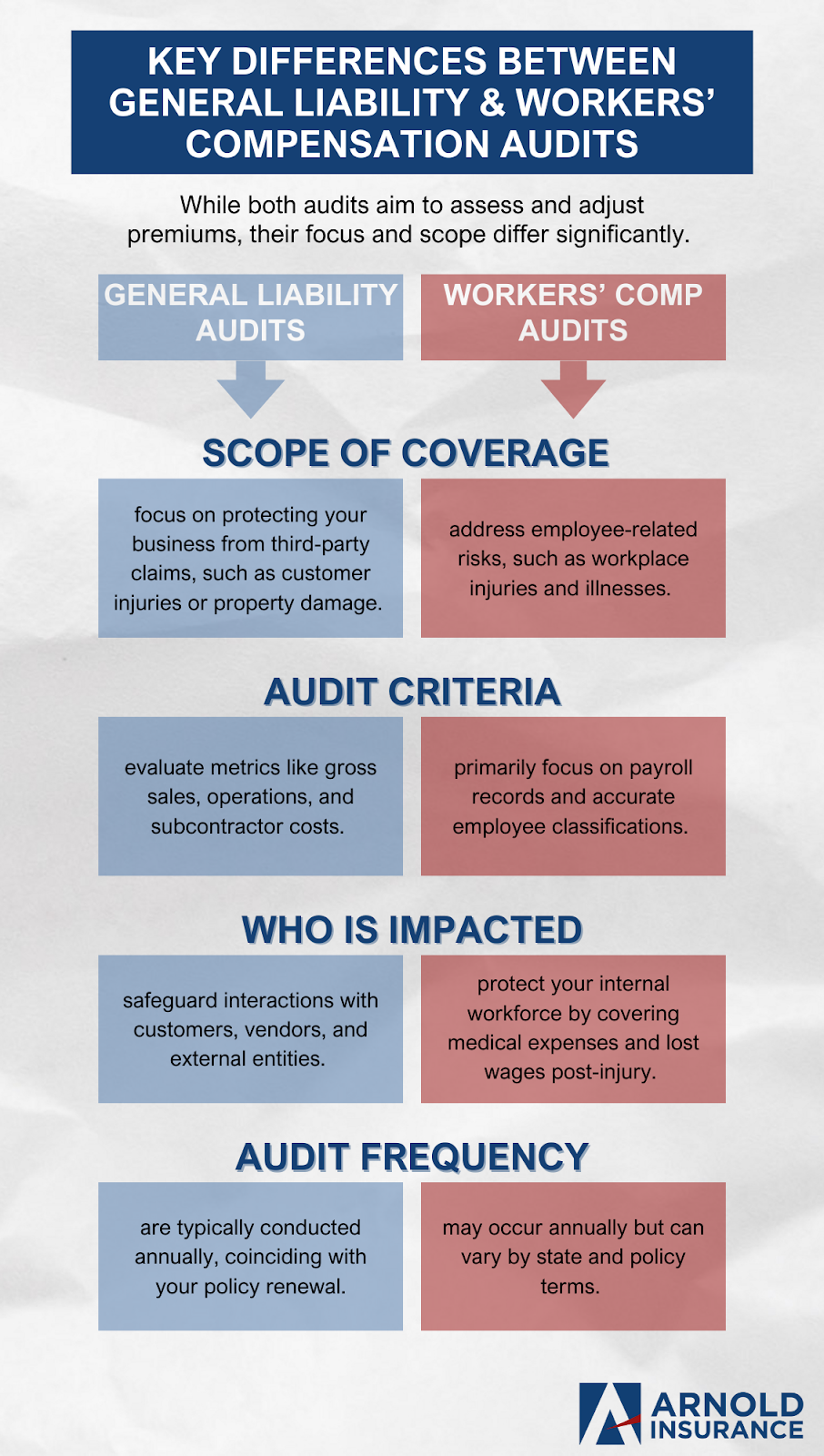

What is a General Liability Insurance Audit?

A general liability insurance audit ensures that your business is paying the appropriate premium based on your actual exposure. Insurers use this process to verify the information provided when the policy was purchased, like estimated revenue or subcontractor costs, matches the actual numbers during the coverage period.

Purpose of a General Liability Audit

The primary goal is to ensure that your business's general liability risk is adequately covered. This type of insurance protects businesses from third-party claims related to bodily injury, property damage, and advertising errors.

What Is Evaluated During the Audit?

Some key factors insurers examine include:

- Gross sales: The total revenue your business has earned during the coverage period.

- Subcontractor costs: Payments to subcontractors that may affect liability risk.

- Employee count and roles, especially for customer-facing positions, which typically carry greater risk.

Why It’s Important

Failing to provide accurate data during the policy period may expose your business. For instance, if your revenue has increased but you haven’t updated your insurer, you could face hefty additional premiums after the audit. On the flip side, providing accurate data allows you to avoid overpaying and ensures your policy offers the right level of protection.

What is a Workers’ Compensation Insurance Audit?

A workers’ compensation insurance audit ensures your business has properly classified employees and reflects accurate payroll figures. Workers’ compensation covers employee injuries or illnesses arising from the job, which makes accurate reporting critical to avoiding penalties.

Purpose of a Workers’ Compensation Audit

The audit confirms whether policy premiums align with actual payroll and employee classifications during the coverage period.

What Is Evaluated During the Audit?

Insurers examine the following:

- Payroll totals: The insurer cross-references your payroll records with reported earnings to determine the appropriate premium.

- Employee classifications: Job roles are analyzed to ensure employees are accurately classified based on the risk associated with their work.

- Independent contractors or subcontractors, as misclassification can lead to fines or uncovered risks.

Why Accurate Classification Matters

Misclassifying employees (e.g., listing a construction worker as an administrative clerk) is a common mistake that can lead to audits, fines, or even denial of claims. A workers’ comp audit provides an opportunity to resolve discrepancies and ensure compliance with regulations.

How to Prepare for Insurance Audits

Understanding the audit process is only half the battle. Proper preparation not only streamlines the process but can also save you money and headaches.

Best Practices for Both Audits

1. Maintain Organized Records- Payroll documents

- Gross sales reports

- Contracts and invoices for subcontractors

- Employee classifications

2. Communicate with Your Insurance Provider

- Ensure your provider explains how the audit will be conducted and what information is required. Staying informed can prevent unnecessary stress.

3. Use an Audit Checklist

- For workers’ compensation, refer to a workers’ comp audit checklist to make sure nothing falls through the cracks. For liability coverage, track gross revenue and subcontractor costs regularly.

4. Review Your Policies Annually

- Business operations evolve. Scheduling annual reviews with your agent not only keeps your premiums accurate but also ensures you are fully protected.

Preparing for these audits doesn’t have to be overwhelming. At Arnold Insurance, we specialize in guiding small businesses and organizations through the complex process of insurance audit preparation. Our expertise helps clients maintain compliance, eliminate guesswork, and reduce audit-related surprises.

Confidence in Audits Means Confidence in Coverage

Navigating general liability and workers’ compensation audits doesn’t have to be intimidating. These audits ensure your insurance premiums are accurate, and most importantly, your coverage aligns with your actual risk exposure.

Avoid penalties, optimize your premiums, and keep your business protected by taking the time to prepare for these audits. If you need expert guidance, Arnold Insurance is here to help. From workers’ comp audit checklists to navigating liability insurance audit tips, our team ensures your business receives tailored support and clear coverage every step of the way.

Start your insurance audit preparation today by contacting Arnold Insurance.

FAQS

Q: What is the purpose of a general liability insurance audit?

A: It ensures your premiums match actual business exposure, based on factors like revenue, subcontractor costs, and employee roles.

Q: Why is a workers’ compensation insurance audit important?

A: It confirms payroll accuracy and proper employee classification, which prevents fines, misclassification errors, and coverage gaps.

Q: How should a business prepare for an insurance audit?

A: Keep payroll records, sales reports, subcontractor invoices, and employee classifications organized, and communicate with your insurer about requirements.

Q: What happens if my business information is inaccurate during an audit?

A: You could face higher premiums, penalties, or denied claims if revenue, payroll, or employee classifications are reported incorrectly.

Q: How often should businesses review their insurance policies?

A: At least once a year to ensure premiums remain accurate and coverage reflects your current operations.